Weekly Insights - Edition 117

This week: Equity breakouts, EM risk sentiment, change in commodity market technicals, global monetary policy pulse, treasuries outlook, stocks vs bonds...

Welcome to the Weekly Insights report! The weekly insights report presents some of the key findings from our institutional research service, providing an entrée experience (in terms of price and size).

Global Markets Monitor - notable developments

Perhaps of most note was the Euro Stoxx 50 index making an initial break higher out of its trading range and through a key resistance level. Somewhat similar, EM equities have been pushing higher as well; turning up off its base. US equities a bit more mixed with small caps and nasdaq pausing at resistance. On sectors, energy and materials have been ticking higher as commodities rebound, financials also gaining, and tech sectors losing ground.

Sovereign bond yields mixed/consolidating, JGB yields being the standout (ticking higher) as the BOJ widened its defacto YCC cap on 10yr yields to 1% (from 50bps). Elsewhere, credit spreads and CDS pricing continue to narrow -- most notably in EM corporates and sovereigns (general improved risk sentiment globally, rebound in commodities, weakening bias in USD, prospect of Fed pause/peak, and signs of a turn in EM policy).

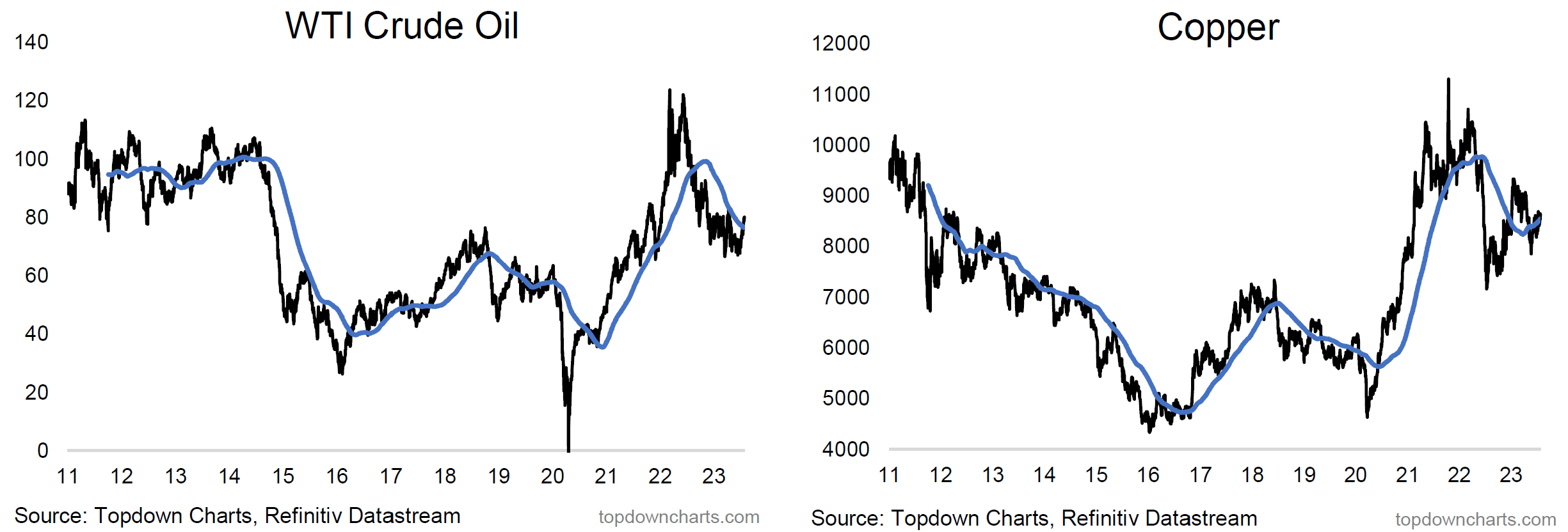

The DXY remains above 100 (but below resistance) after an initial so-far failed break lower, EMFX meanwhile trading a tight range. Commodities index turning higher, driven most notably by an uptick in energy prices (follows general improvement in commodities e.g. higher lows in copper and gold, rebound in agri).

Market themes: Commodities bear no more...

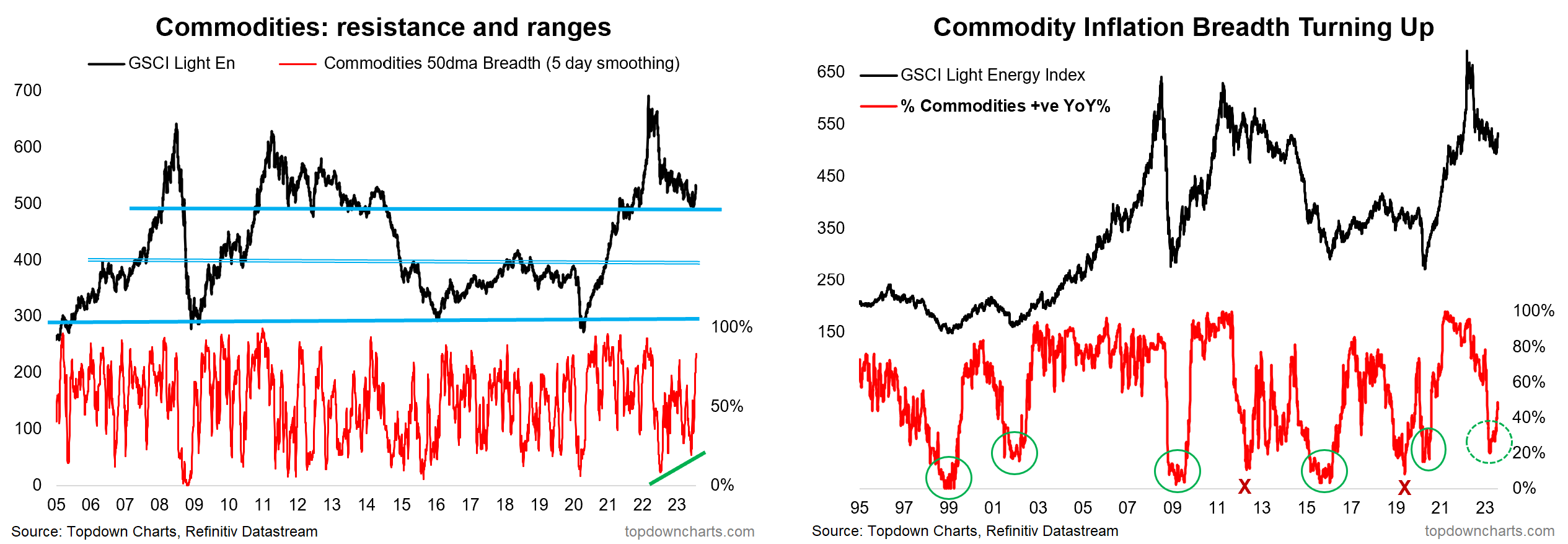

-Commodity technicals have improved significantly

--bullish breadth divergence, index rebounding off support

--medium-term breadth indicator pointing to bullish turning point

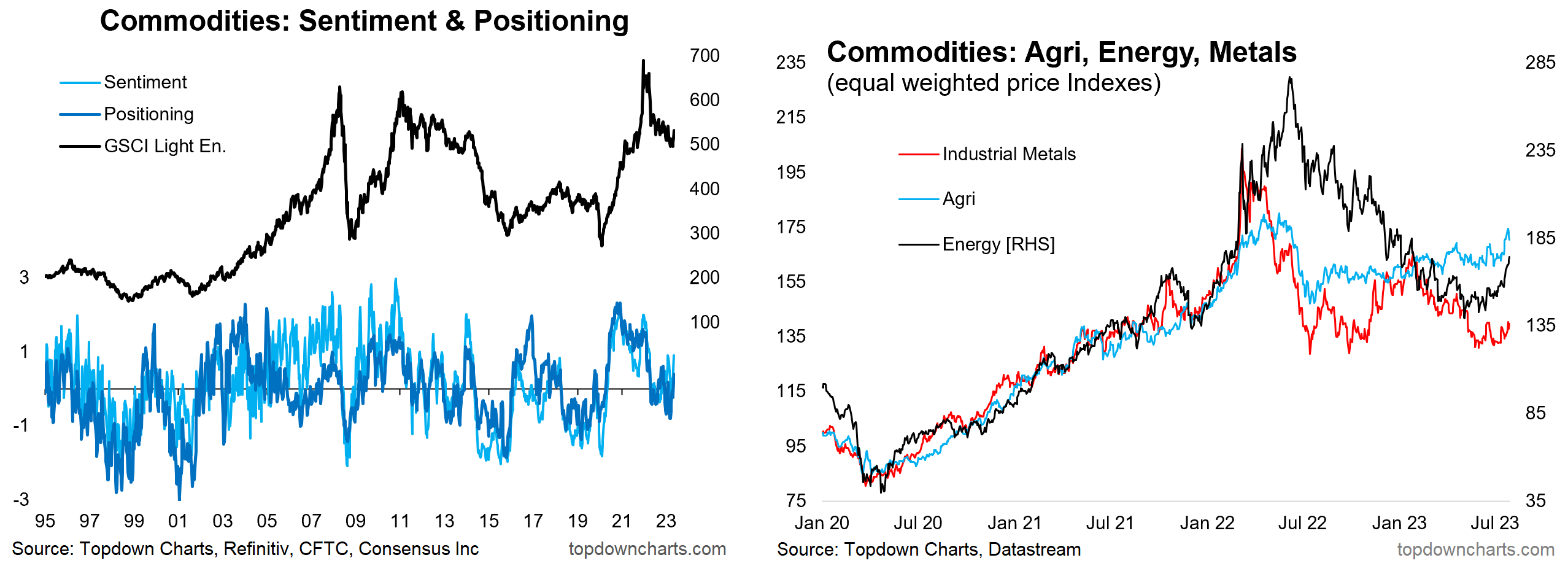

--sentiment/positioning turning up after a material reset

--major groups within commodities turning up/basing

-Hence best to remove the previous bearish view on commodities (which was originally established in early May last year).

--possible fundamental supports could come from: China stimulus, weaker USD, reset in valuations, still low pace of capex (ongoing underinvestment in supply), and thematic drivers.

---albeit not quite ready to turn bullish commodities (need to see more confirmation in the technicals + macro first).

Commodity technicals have improved notably in the last few weeks, with the GSCI light energy index rebounding from support with what looks like a bullish divergence on the 50dma breadth chart (breadth indicator making a higher low vs lower low in the index -- a useful turning point signal). Similarly, the commodity inflation breadth indicator (proportion of commodities with positive YoY % change aka "inflation") is turning up after previously collapsing... which has been a major medium-term bull signal 5 out of 7 times over the past couple decades.

Also of interest is sentiment and positioning turning up after a healthy reset (albeit not as extreme as in some of the previous major market bottoms e.g. 98,01,08,15,20), and at a time when fund manager surveys show consensus is now underweight commodities (having been previously consensus overweight around the peak in 2022). Looking across the major groups, agri is picking up steam, energy turning up off the lows, and industrial metals basing.

On the Radar

Macro & Markets: This week is rich in macro data with basically all the PMIs for July due out (timely update on the global economy), the increasingly-watched Fed loan officer survey, rate decisions from the RBA and BoE, and payrolls.

In markets, the 10yr yield is pulling back below 4% again, DXY tracking around short-term resistance (still above 100), gold ranging (locked in a higher low), WTI crude pushing resistance ~81, and stocks ticking higher...

Research Agenda: This week obviously will be digesting the various macro news, but also working on the Monthly pack and reviewing the big picture outlook.

Weekly Macro Themes Report - key points

1. Global Monetary Policy Pulse: pivots, peaks, and the monetary wall…

So far in 2023 I count 152 interest rate hikes across 59 central banks (and that’s on top of more than 300 hikes in 2023)… vs 31 interest rate cuts across now 15 central banks who’ve moved into rate cutting mode.

The pivot to rate cuts is mostly at the fringes so far, the smaller/developing country banks, but it’s also making its way across emerging market central banks, and edging ever closer to the mainstream central banks.

For the mainstream though it’s more tightening, and that only adds to the growing “monetary wall” looming in H2 and 2024 (the various monetary + central bank related leading indicators point to sharp headwinds, strong recession signal).

Equity markets are so far shrugging-off record QT and rate hikes, but having said that, looking at the 2000 + 2007 peaks, it wasn’t the rate hike phase as such, it was when rate hikes were done that markets came undone.

In terms of when we should expect a peak, EM already look to be well into that process with yields peaked and cash rates making an initial peak. But Developed Markets however continue to push higher on cash rates and bond yields.

Bottom line: Seeing a pivot in rates at the edges, a peak for EM, and continued push higher by DM; and overall unprecedented monetary tightening presenting a “monetary wall”.

2. Treasuries: cheap value, excess pessimism, but still mixed signals on macro/technicals…

Developed sovereign bond yield breadth has been ticking higher, with a bullish continuation pattern flagging the risk of further upside in yields.

On the other hand, historically the next few months have typically been the strongest part of the year for treasuries.

The PMIs continue to point to downside for treasury yields, but perhaps just as there was a long lag on the way up, maybe a long lag on the way down too.

Meanwhile the long-term rate of inflation and nominal growth models point to a little further upside in government bond yields.

So there is a clear tension between evidence for higher vs lower yields.

In the background, treasuries still showing up as cheap (albeit not extreme cheap), and sentiment remains consensus bearish on treasuries.

The bull case remains credible, but it likely requires either a last cathartic push higher in yields, or a more undeniable turn down in the macro.

Bottom line: Remain bullish treasuries given valuations, sentiment, and certain aspects on the technicals + macro, but acknowledge lingering evidence flagging upside risk to yields.

3. Stocks vs Bonds: technically bullish, fundamentally bearish…

In terms of the technicals, it’s a clear bullish picture for stocks vs bonds as the US S&P500 vs treasuries ratio breaks out from trading range to new all time highs.

Relative sentiment is also pushing higher, getting closer to, but not quite yet at extremes. And meanwhile the stock/bond ratio has been trending higher for EM + DM as well. So from a technical standpoint it’s a bad idea to be bearish stock/bond.

But then if we look at valuations, we see the relative value indicator for stocks vs bonds at the highest point since 2018 (which as it happens saw a significant correction triggered by rising bond yields).

Absolute valuations are also ticking higher, with US equity valuations surpassing the pre-covid highs. Meanwhile, bonds are cheap in absolute terms (and relative to stocks), so the odds from a valuation standpoint favour bonds.

On the macro front, the relative performance of stocks vs bonds stands at odds with the leading indicators and the coincident cycle indicators.

Hence, I continue to reluctantly cling to my bearish view on stocks vs bonds as bullish technicals for now beat bearish fundamentals. If I had no view previously I might be neutral, but just looking at the risk outlook, I think it requires strong confounding evidence to chase price and ignore the macro/value risks.

Bottom line: While the technicals are clearly bullish, the macro + value factors point to poor risk/reward for stocks vs bonds.

Ideas Inventory - Updated to 31 July 2023

(Table of Current live Ideas/Themes where an explicit view has been issued)