Weekly Insights - Preview and Chart of the Week

Here's what we covered in the latest report...

This email provides a look at what we covered in the latest Weekly Insights report

The weekly insights report presents some of the key findings from our institutional research service, providing an entrée experience (in terms of price and size).

Topics covered in the latest Weekly Insights Report:

Treasuries: why the risks are still skewed to the upside for bond yields.

US Dollar: thoughts on the near-term outlook (and medium-longer term view).

Commodities: a review of the short-term risks vs longer-term bull case.

European Equities: why we remain bullish on the outlook there.

CMA Update: implications of upward revisions to growth expectations.

REITs: highlighting the reset in sentiment/technicals for this sector.

Subscribe now to get instant access to the report so you can check out the details around these themes, as well as gaining access to the full archive of reports.

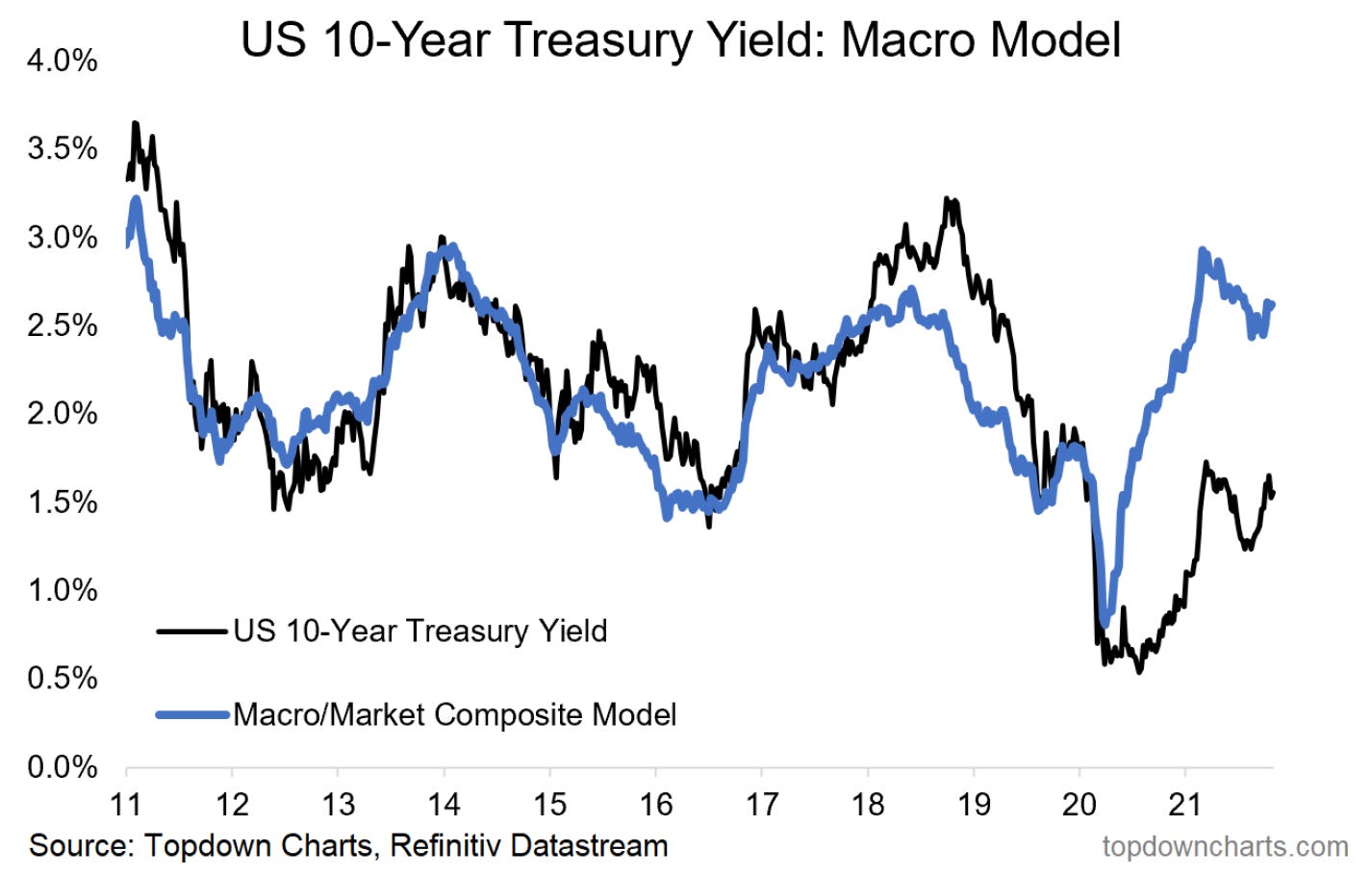

Chart of the Week - Bond Market Risk Watch

Treasuries Macro/Market Model: The Fed may well be able to deliver a “dovish taper” by announcing it on Nov 3rd - but scheduling it to start later, and running it over a long period, and being very much data-dependent. The last thing they will want is to spook markets (but you don’t always get what you want!).

The risk is that whatever they do, the market makes its mind up that it’s time for yields to move higher. The chart below lays out the risk quite plainly… My 6-factor macro/market composite model is still pointing to US 10-year treasury yields in the order of 2.5% — almost a full percentage point higher than where it sits as of the time of writing...

If you haven’t already, be sure to subscribe to our paid service so that you can receive the full reports ongoing (along with full access to the archives, monthly asset allocation review, and Q&A).

Thanks for your interest. Feedback and thoughts welcome.

Sincerely,

Callum Thomas

Head of Research and Founder at Topdown Charts

Follow me on Twitter

Connect on LinkedIn